This post was published 6/5/2020 and edited on 6/16/2020.

I said I was going to rave about Marcus, so here we are.

As mentioned in my previous finance post, we opened up an 11mo no penalty CD and a High-Yield Savings Account (HYSA) with Marcus by Goldman Sachs. If you haven’t read it yet, check it out to find out our thought process behind choosing those specific accounts. If you’re interested in opening up your own, click here for the CD and click here for the HYSA.

This post was published on 5/30/2020 and last edited on 6/16/2020.

Click here to skip this post and just read what we ended up opening.

In my previous post I wrote about researching the best CD in the market at present because we were interested in opening up a new one.

However, what we found out during the process of deliberation between Ally and Marcus, was that Marcus also have a High-Yield Savings Account (HYSA) that offers 1.30% APY. Also if you don’t live in California, there are other banks that give much higher APY %’s for their HYSAs. What the heck! So I guess if you live in another state you should look into what’s best for you there.

Anyways, let’s go back to the 1.30% APY that we actually have access to. This is higher than most of the no-penalty CDs!

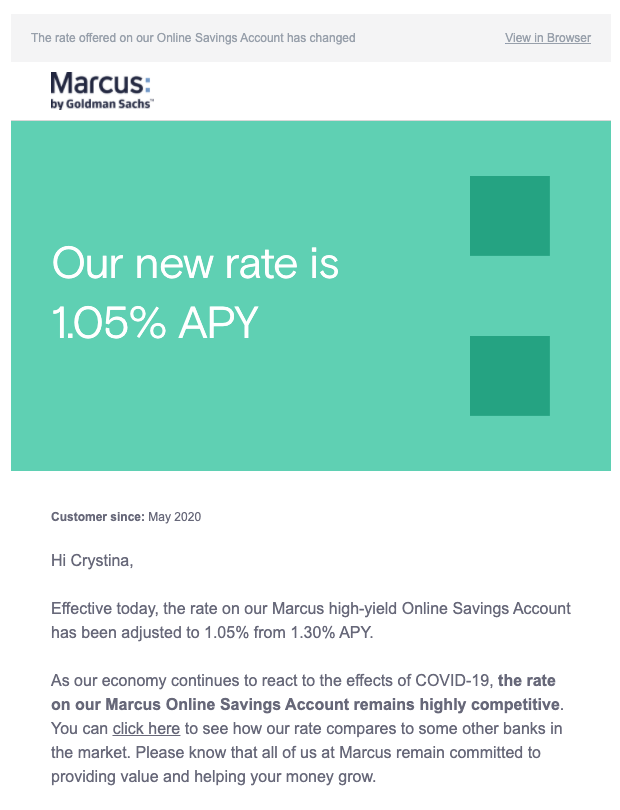

But there’s also a reason for this: this high APY rate will fluctuate as the Federal Reserve’s interest rates rise or decrease, so you aren’t guaranteed that rate will remain. The Marcus representative I spoke to advised that unfortunately they do not send out emails to notify their customers if the APY rate decreases.

Edit: Turns out this is untrue and they do actually notify customers if their rates change! I literally just received this email:

As such, we had to decide if we should still open up a CD to lock in the APY rate, or if we should just put the investment into a HYSA instead. Also, if we were still going to open up a CD, should we open a 7mo or 11mo one? By this time, I already had my heart set on Marcus by Goldman Sachs, so all of these are related to what they offer. Here’s our thought process:

This post was published on 26th May 2020 and edited on 27th May 2020.

The Basics

CD stands for “Certificate of Deposit”, meaning you deposit a sum of money into a bank that must remain in the bank for a fixed term, in order for you to receive a certain percentage of interest on your money. Anyone who has more than $1k just hanging out in their bank account should consider opening up a CD to get a higher interest rate.

…Which is why I looked into it. Our interest savings account is on 0.01% APY whereas your average no-penalty CD is offering 1.00% APY – that’s 100x higher than what I’m getting with my bank right now. (Note: “APY” just means the amount of interest you’ll earn on your money over period of 1yr, compounding annually. It stands for “Annual Percentage Yield”.)

Typically if you withdraw the money early, you will be charged penalties of varying severity depending on the bank. I looked into current CD’s being offered at the highest rates of interest, that will allow you to close it down and take out your money (and interest) after just 7 days, with zero penalties.

Now there are certainly longer-term CDs that offer higher APY’s, but you never know when you’re going to need your money back, and right now the interest rates are very low due to economic instability from COVID, so I do not recommend getting stuck in a long-term CD. This is true especially if you have a larger sum of money to invest, and if you don’t have that much to invest, the extra 0.1-0.3% APY won’t make much of a difference anyway.

But why should you trust me, a random person on the internet? You don’t have to, but I’ve spent hours researching this because I am not super well-versed in all of this investment/financial jargon malarky, and I’ve decided to summarise my key findings in lay-mans terms here to save you time from doing it yourself. I do also have a Business Studies degree from one of the top UK universities, if that helps.