This post was published on 5/30/2020 and last edited on 6/16/2020.

Click here to skip this post and just read what we ended up opening.

In my previous post I wrote about researching the best CD in the market at present because we were interested in opening up a new one.

However, what we found out during the process of deliberation between Ally and Marcus, was that Marcus also have a High-Yield Savings Account (HYSA) that offers 1.30% APY. Also if you don’t live in California, there are other banks that give much higher APY %’s for their HYSAs. What the heck! So I guess if you live in another state you should look into what’s best for you there.

Anyways, let’s go back to the 1.30% APY that we actually have access to. This is higher than most of the no-penalty CDs!

But there’s also a reason for this: this high APY rate will fluctuate as the Federal Reserve’s interest rates rise or decrease, so you aren’t guaranteed that rate will remain. The Marcus representative I spoke to advised that unfortunately they do not send out emails to notify their customers if the APY rate decreases.

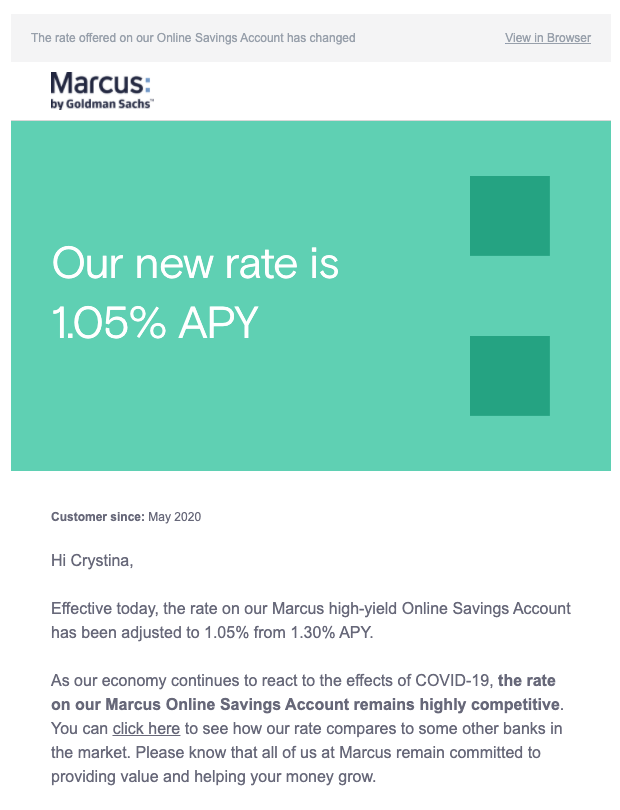

Edit: Turns out this is untrue and they do actually notify customers if their rates change! I literally just received this email:

As such, we had to decide if we should still open up a CD to lock in the APY rate, or if we should just put the investment into a HYSA instead. Also, if we were still going to open up a CD, should we open a 7mo or 11mo one? By this time, I already had my heart set on Marcus by Goldman Sachs, so all of these are related to what they offer. Here’s our thought process:

CD vs High-Yield Savings

| Product | 7mo CD | 11mo CD | High-Yield Savings |

| APY | 1.30% | 1.20% | 1.30% |

| Term | 7 months | 11 months | None |

| Rate locked? | Yes | Yes | No |

| Can withdraw / deposit money? | No withdrawals allowed. Deposits allowed up to $500* | No withdrawals allowed. Deposits allowed up to $500* | Yes – unlimited |

* If you don’t have more than $500 to deposit into your CD in one go, you may deposit money until your CD hits $500, then you may not make additional deposits. You can of course deposit more than $500 in one go, then leave the total sum there until maturity or until you close it down. This is what we planned to do.

Note that all of the above options lock your money in for 7 days before you can access it again (the HYSA will allow you to continue depositing, but you cannot withdraw until the 7 days are up).

7mo vs 11mo CD

If interest rates decrease before 7mo

Our HYSA rate will decrease, our 7mo CD will be locked in but once it matures we’ll have to renew at a much lower interest rate. 11mo CD would be best.

If interest rates decrease between 7 – 11mo

Our HYSA rate will decrease, our 7mo CD would have matured and we may no longer have a good rate to renew it at. 11mo CD would be best.

If interest rates decrease after 11mo

Our assumption is that interest rates will increase after 11mo, because hopefully we’ll be past the pandemic and the economy will be recovering by this time next year.

If interest rates increase at any time

Our HYSA rate may increase, we can shut down either of the CD’s and open a new CD at the newer rate. This is unlikely to happen and would also require us to keep our eyes peeled at interest rates, but I’m happy to do that.

You may be wondering why the rate is higher for the 7mo CD. My best guess is because it’s fixed for a shorter period of time.

Banks want to protect themselves from further significant interest rate decreases from the Federal Reserve in 6-12mo’s time, so if Marcus locks themselves in to a 1.30% APY for you, they’ll be losing money by keeping you at a higher rate when they have no guarantee that you’ll keep your money in their CD.

When you invest your money in their bank, they will use your money to make investments of their own. Their goal is to get returns higher than the APY rates they are offering you. If they don’t know how long they can play with your money for, they run the risk of losing out on some of their own investments because they have to return your money back to you. That’s why you’ll always have a higher APY with fixed term CDs.

On the other hand, if the interest rate increases, you will also have the flexibility to close down the CD and open up a new one at the higher interest rate.

Ultimately, Jacky and I worked out that the returns we’d receive on a 11mo CD at 1.20% APY would be higher than if we’d invested the money in a 7mo CD at 1.30% APY and lost the rate. At the same time, the amount we’d “lose” in interest during that time would not be significant enough given our investment.

Finally, we decided that since we were going to continue saving up over the months, we wanted to put any extra cash we had into a savings account that would give us the highest returns whilst offering us flexibility to add or take from it as and when we needed…

What We Opened

Given all of this, you’ll not be at all surprised to hear that we ended up opening both a Marcus 11mo no penalty CD and a Marcus High-Yield Savings Account. We put what we’d previously decided to set aside into the CD and put some additional spare cash into the HYSA.

Honestly I am so impressed with Marcus. It’s been ideal for our needs in this particular case. I’m actually going to dedicate an entire blog post on why they’re so great. Hopefully they don’t disappoint me after this :p

I hope this post was insightful and maybe even inspired you to review your own finances. Let me know if it did!